Our mission is to help computational modelers develop, document, and share their computational models in accordance with community standards and good open science and software engineering practices. Model authors can publish their model source code in the Computational Model Library with narrative documentation as well as metadata that supports open science and emerging norms that facilitate software citation, computational reproducibility / frictionless reuse, and interoperability. Model authors can also request private peer review of their computational models. Models that pass peer review receive a DOI once published.

All users of models published in the library must cite model authors when they use and benefit from their code.

Please check out our model publishing tutorial and feel free to contact us if you have any questions or concerns about publishing your model(s) in the Computational Model Library.

Displaying 10 of 1149 results for "J A Cuesta" clear search

An agent-based model to simulate meat consumption behaviour of consumers in Britain

Andrea Scalco | Published Friday, October 18, 2019The current rate of production and consumption of meat poses a problem both to peoples’ health and to the environment. This work aims to develop a simulation of peoples’ meat consumption behaviour in Britain using agent-based modelling. The agents represent individual consumers. The key variables that characterise agents include sex, age, monthly income, perception of the living cost, and concerns about the impact of meat on the environment, health, and animal welfare. A process of peer influence is modelled with respect to the agents’ concerns. Influence spreads across two eating networks (i.e. co-workers and household members) depending on the time of day, day of the week, and agents’ employment status. Data from a representative sample of British consumers is used to empirically ground the model. Different experiments are run simulating interventions of application of social marketing campaigns and a rise in price of meat. The main outcome is the average weekly consumption of meat per consumer. A secondary outcome is the likelihood of eating meat.

MASTOC - A Multi-Agent System of the Tragedy Of The Commons

Julia Schindler | Published Tuesday, November 30, 2010 | Last modified Saturday, April 27, 2013MASTOC is a replication of the Tragedy of the Commons by G. Hardin, programmed in NetLogo 4.0.4, based on behavioral game theory and Nash solution.

John Q. Public (JQP): A Model of Political Judgment and Behavior

Sung-Youn Kim | Published Monday, March 14, 2011 | Last modified Saturday, April 27, 2013The model integrates major theories of political judgment and behavior within the classical cognitive paradigm embedded in the ACT-R cognitive architecture. It models preferences and beliefs of political candidates, parties, and groups.

A simple behavioral model predicts the emergence of complex animal hierarchies

Takao Sasaki Zachary Joseph Shaffer Stephen Pratt Clint A Penick Jürgen Liebig | Published Tuesday, December 22, 2015We used our model to test how different combinations of dominance interactions present in H. saltator could result in linear, despotic, or shared hierarchies.

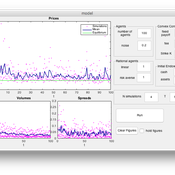

An Agent Based Model for implementing a double auction financial market

Annalisa Fabretti | Published Thursday, April 14, 2016The model implements a double auction financial markets with two types of agents: rational and noise. The model aims to study the impact of different compensation structure on the market stability and market quantities as prices, volumes, spreads.

Peer reviewed Simulating the Economic Impact of Boko Haram on a Cameroonian Floodplain

Mark Moritz Nathaniel Henry Sarah Laborde | Published Saturday, October 22, 2016 | Last modified Wednesday, June 07, 2017This model examines the potential impact of market collapse on the economy and demography of fishing households in the Logone Floodplain, Cameroon.

Peer reviewed A Model of Global Diversity and Local Consensus in Status Beliefs

André Grow Andreas Flache Rafael Wittek | Published Wednesday, March 01, 2017 | Last modified Wednesday, October 25, 2017This model makes it possible to explore how network clustering and resistance to changing existing status beliefs might affect the spontaneous emergence and diffusion of such beliefs as described by status construction theory.

A Pastoral Stoking Strategy Model with Fodder Import and Loan Scenarios

Yanbo Li | Published Tuesday, December 24, 2019This model was built to estimate the impacts of exogenous fodder input and credit loans services on livelihood, rangeland health and profits of pastoral production in a small holder pastoral household in the arid steppe rangeland of Inner Mongolia, China. The model simulated the long-term dynamic of herd size and structure, the forage demand and supply, the cash flow, and the situation of loan debt under three different stocking strategies: (1) No external fodder input, (2) fodders were only imported when natural disaster occurred, and (3) frequent import of external fodder, with different amount of available credit loans. Monte-Carlo method was used to address the influence of climate variability.

HyperMu’NmGA - Effect of Hypermutation Cycles in a NetLogo Minimal Genetic Algorithm

Cosimo Leuci | Published Tuesday, October 27, 2020 | Last modified Sunday, July 31, 2022A minimal genetic algorithm was previously developed in order to solve an elementary arithmetic problem. It has been modified to explore the effect of a mutator gene and the consequent entrance into a hypermutation state. The phenomenon seems relevant in some types of tumorigenesis and in a more general way, in cells and tissues submitted to chronic sublethal environmental or genomic stress.

For a long time, some scholars suppose that organisms speed up their own evolution by varying mutation rate, but evolutionary biologists are not convinced that evolution can select a mechanism promoting more (often harmful) mutations looking forward to an environmental challenge.

The model aims to shed light on these controversial points of view and it provides also the features required to check the role of sex and genetic recombination in the mutator genes diffusion.

Gossip and competitive altruism support cooperation in a Public Good Game

danielevilone | Published Friday, April 16, 2021Here we share the raw results of the social experiments of the paper “Gossip and competitive altruism support cooperation in a Public Good Game” by Giardini, Vilone, Sánchez, Antonioni, under review for Philosophical Transactions B. The experiment is thoroughly described there, in the following we summarize the main features of the experimental setup. The authors are available for further clarifications if requested.

Participants were recruited from the LINEEX subjects pool (University of Valencia Experimental Economics lab). 160 participants mean age = 21.7 years; 89 female) took part in this study in return for a flat payment of 5 EUR and the opportunity to earn an additional payment ranging from 8 to 16 EUR (mean total payment = 17.5 EUR). 80 subjects, divided into 5 groups of 16, took part in the competitive treatment while other 80 subjects participated in the non-competitive treatment. Laboratory experiments were conducted at LINEEX on September 16th and 17th, 2015.

Displaying 10 of 1149 results for "J A Cuesta" clear search